Finding value in frontier African markets

Nick Ndiritu

Across corporate boardrooms in South Africa, a number of management teams and institutional investors are grappling with a vexing question: Is investing in frontier African markets worth the hassle? Nick Ndiritu explains how Allan Gray has wrestled with the uncertainty of investing in frontier markets.

Established South African industry leaders are struggling with the well-known challenges of doing business in [the rest of] Africa. From Nigeria to Uganda, the regulatory challenges faced by telecommunications company MTN resemble a cruel game of whack-a-mole: As soon as you fix one, another appears. Africa’s leading retailer, Shoprite, reported its largest earnings decline in over a decade, citing currency devaluation in Angola as the cause. In the financial services sector, Liberty Holdings is looking to sell down loss-making African operations in asset management and health.

Newer entrants with less established African footprints, initially drawn to the continent’s alluring growth prospects, are scaling back their ambitions. South African property companies Attacq and Hyprop recently impaired the value of their ‘rest of Africa’ assets and are looking to exit or pare down a joint venture that owns shopping malls in Ghana, Zambia and Nigeria. Most of their tenants are South African retailers who have scaled back their Africa expansion plans and are unlikely to renew their leases. Their concerns are valid. In 2013, retailer Woolworths exited Nigeria, citing high rental costs and supply chain challenges as reasons. In 2016, fashion chain Truworths also exited Nigeria due to high rentals and import restrictions.

There are success stories

On the other hand, there are compelling examples of South African corporates who have thrived on the continent. Standard Bank’s footprint in 20 African markets is unrivalled. Their ‘rest of Africa’ business is lucrative, earning a 24% return on equity (ROE) compared to the group’s 18% ROE, and is now contributing a meaningful 29% to group earnings.

MTN’s operations in Nigeria are thriving despite all the regulatory hullabaloo. At the end of 2018, revenues grew by 17%, with an 11% increase in their subscriber base to 58 million, and their EBITDA (earnings before interest, taxes, depreciations and amortisation) margin expanded by 4.5 percentage points (pp) to 43.5%, excluding once-off regulatory payments. Shoprite remains a formidable competitor in Africa’s retail landscape despite short-term macroeconomic challenges in Angola and Nigeria. Battlefield scars are inevitable as these companies diligently build their competitive positioning through the ups and downs.

South African corporates have also dispelled any doubts that new market entrants can crack the challenging business environment in Nigeria. Brewer SABMiller (prior to its merger with Anheuser-Busch InBev) entered Nigeria’s beer market in 2009 and later invested US$100m to build a brewery in the city of Onitsha. They pursued a differentiated regional marketing strategy, championing regional brands which resonated with the traditions and culture of the local communities. This strategy also avoided fierce nationwide competition with dominant Heineken and Diageo.

SABMiller also specifically addressed affordability, focusing on the number of minutes worked to earn a core beer. The company considers a beer to be affordable at 30 minutes, but the majority of the population in Nigeria is in the low- to mid-income range, where an individual needs to work for 72 to 140 minutes to earn a beer. Cheaper pricing expanded their reach into the value-conscious segment, at the expense of peers like Diageo, who have stumbled during Nigeria’s recent economic slump.

The results have been impressive, with SABMiller garnering a 22% market share of Nigeria’s beer market. AB InBev is building on SABMiller’s groundwork, recently commissioning a US$250m brewery to meet growing demand and now expanding from a regional to a nationwide distribution footprint. At a time when others may be considering exit options, AB InBev is unabashedly betting on Nigeria’s beer market.

It is not easy doing business in Africa

These examples of success and failure highlight the fallacy of sweeping narratives. The insistent story of a rising Africa underplays the challenges of doing business on the continent. Progress in changing the business environment has been uneven. One objective measure to track this progress is the World Bank’s Doing Business rankings, which indicate the ease of doing business in 190 countries. They score each country based on various indicators that help determine the efficacy of the business environment: How easy is it to start a business, deal with construction permits, get electricity, register property, get credit, pay taxes, trade across borders, enforce contracts and resolve insolvency. Using the same standard everywhere enables comparability across economies.

Graph 1 shows the ease of doing business scores for select African countries over the last five years. In 2015, South Africa was ranked 43rd out of 189 economies, and was on a par with Rwanda as one of Africa’s top-ranked economies. By 2019, South Africa has fallen behind, with the Doing Business score having increased by only 2 pp compared to Rwanda’s 10 pp improvement. Over this period, Kenya has made the most progress, with a 16 pp gain and jumping from a rank of 136 to 61. Nigeria has also made progress, but from a low base of being ranked 170th to 146th.

In aggregate, these scores highlight that in most frontier markets, companies seeking opportunities there are barely welcomed by smooth and efficient functioning of regulators, tax authorities and judiciaries, among others. These challenges aren’t new or unique to Africa, but according to the Doing Business 2019 report, sub-Saharan Africa has been the region with the highest number of reforms each year since 2012. This past year, they captured a record 107 reforms across 40 economies in sub-Saharan Africa. Countries eager to lure investment are undertaking measurable pro-business reforms.

Establishing a competitive edge remains important

Painting the Africa narrative with broad brushes also obscures the role of competition. There will always be winners and losers. Successful market leaders are honing their strategies and ability to compete effectively despite the well-known challenges.

Take the case of Nestlé in Nigeria. To critics, Nigeria’s emerging consumer class is elusive, premised on an oil-dependent economy: Any downswings in oil markets trickle down to constrain household consumption patterns. Undeterred, Nestlé has operated in Nigeria for close to 60 years, selling an ever-growing basket of consumer goods. The competitive environment has intensified in practically all their product categories and brands – sometimes new entrants, and in other cases, existing companies expanding into other categories.

Their competitive edge has come from building a distribution chain that delivers their products to over 300 000 points of sale across a country renowned for poor infrastructure. Modern retailing formats (e.g. supermarkets) account for less than 2% of Nestlé’s sales. Nearly 80% of their raw materials are sourced locally, providing some relief from import restrictions and currency fluctuations. In addition, through the ups and downs, they have invested in building local products like Maggi seasoning cubes, which has limited import substitution based on the purchasing preferences of generations of discerning Nigerian taste buds.

In 2018, which was a difficult year for many consumer goods companies in Nigeria, Nestlé grew earnings by 28% and expanded EBITDA margins by 150 basis points to 27%, the highest on record over the last two decades. Nestlé’s five-year average ROE is an astounding 65%, and this during a period of significant macroeconomic challenges in Nigeria.

Our investment approach

As institutional investors in Africa’s frontier capital markets over the past decade, we have wrestled with uncertainty driven by macroeconomic factors, and we have had to contend with periods of illiquidity in currency markets. From our experience, the most critical driver of long-term investment returns is finding great businesses with a competitive edge and trading at a discount to our estimate of intrinsic value. Asset prices tend to be heavily discounted when sentiment is negative during periods of uncertainty, presenting an attractive buying opportunity for long-term investors. Having the patience and courage to follow this contrarian approach often yields attractive long-term returns.

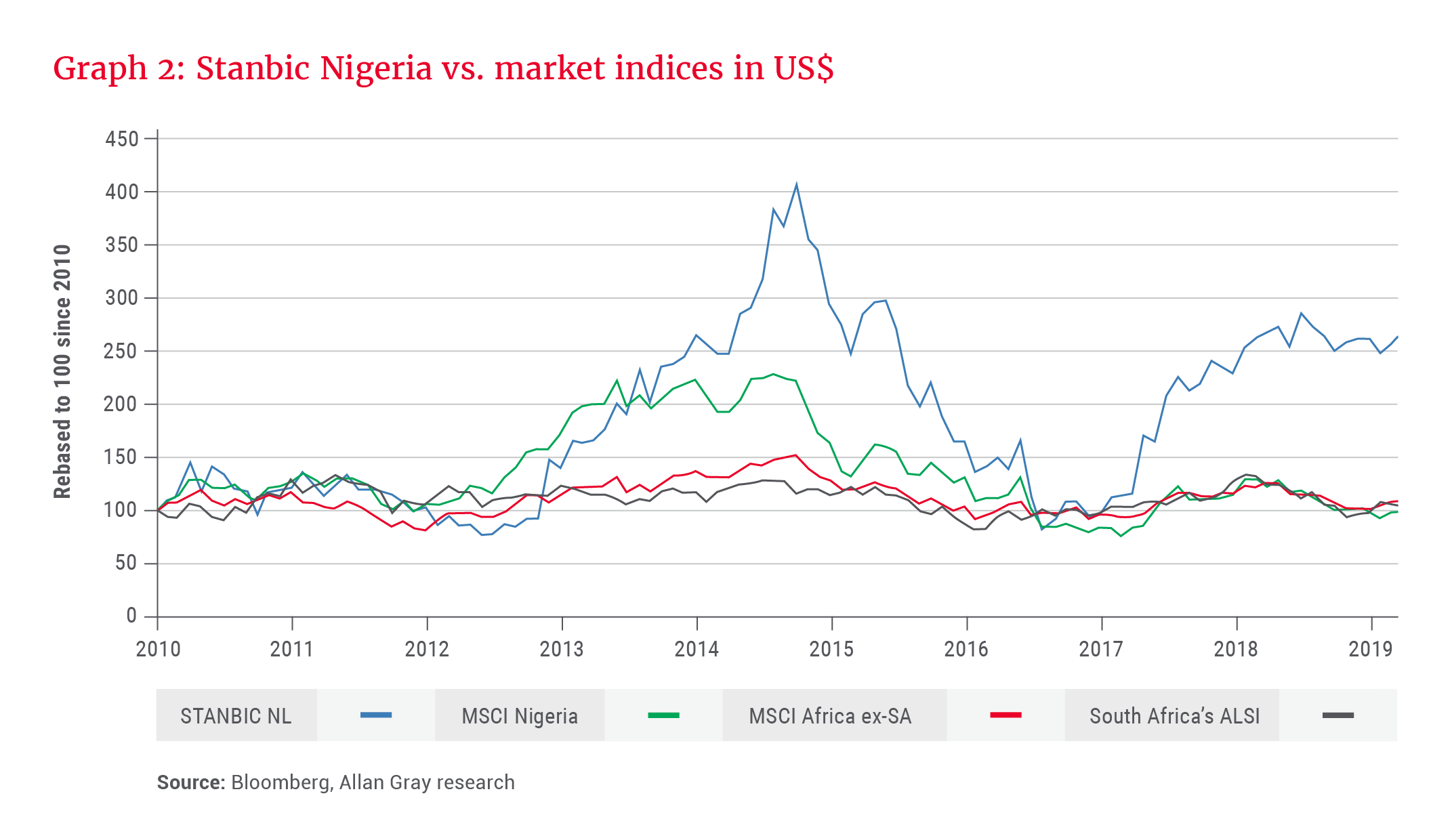

As an illustration, Graph 2 shows the US dollar returns for various market indices relative to Standard Bank’s listed subsidiary in Nigeria, Stanbic IBTC. From 2010 to March 2019, South Africa’s FTSE/JSE All Share Index (ALSI) has been flat in US dollars, barely outperforming MSCI Nigeria and slightly behind MSCI Africa ex-SA. Over this period, Stanbic IBTC has outperformed, but with noticeably higher volatility.

At the peak in 2014, Stanbic IBTC was trading at a 15.2x price-to-earnings (PE) ratio and a 3.3x price-to-book (PB) ratio, which was above our estimate of fair value. Subsequently, oil prices collapsed, and the macro outlook was bleak. Stanbic IBTC also faced heightened regulatory risks. In October 2015, Nigeria’s Financial Reporting Council suspended its chairman, CEO and two directors over allegations that the company had misstated financial statements related mainly to the accrual of franchise fees. The dispute was finally resolved in December 2016, but the lengthy delay prevented the company from releasing financial statements for the 2015 financial year to September 2016.

Despite the distraction from external risk factors, Stanbic IBTC’s management continued to enhance their strong competitive positioning in Nigeria’s pension fund industry. The company’s market share of Nigeria’s pension fund assets has risen to 31% by the end of 2018, up from 24% in 2010. Stanbic IBTC has grown its market share of retirement savings accounts to 21% from 18% in 2010. The company has a top-rated corporate and investment banking franchise and has steadily built a competitive retail banking franchise. It generated a 34% ROE in 2018, bouncing back strongly from Nigeria’s economic slump in 2015, when it generated 13% ROE.

Stanbic IBTC’s share price also bounced back strongly in 2017 as the macro outlook improved after the introduction of a new foreign exchange regime and a steady recovery in oil production and prices. More recently, investors’ concerns about Nigeria’s outlook have resurfaced, but Stanbic IBTC’s long-term prospects are still very attractive. At the end of 2018, Nigeria had 8.4 million retirement savings accounts relative to the estimated 70 million working-age adults. Pension fund assets have risen to US$24bn, which is a paltry 6% of GDP compared to 57% in South Africa and 135% in the US. The company is attractively priced at 6.5x PE, 2.0x PB and 5.8% dividend yield for a market leader with a trusted brand in a promising industry. As long-term investors, Stanbic IBTC is one of our top holdings in Africa and we are prepared to wait through the inevitable periods of economic and political uncertainty.

Conclusion

The challenges of operating in Africa aren’t new or exceptional. Multiple global companies have steadily built thriving businesses in countries across the continent: Unilever, Nestlé, MTN, Shoprite and Standard Bank. Undoubtedly, there are countless others that didn’t survive. What differentiates the winners in frontier markets? From Lagos to Hanoi, success often owes much to the openness and willingness to adapt business models and products to fit constrained household budgets and appeal to the familiar yet aspirational ways of life.

We continue to find attractively valued opportunities and believe frontier African markets are well-suited to a patient, contrarian investment approach.

Nick Ndiritu is a portfolio manager for the Allan Gray Africa ex-SA Equity Fund and Africa ex-SA Bond Fund.